Kinexys as the cash rail: what J.P. Morgan's tokenized Treasury pilot actually proves.

The press release in a single paragraph.

That paragraph contains the entire pilot. Most of what matters about this transaction sits inside its hedges. The rest of this piece pulls each piece apart.

Six entities, two worlds, one seam.

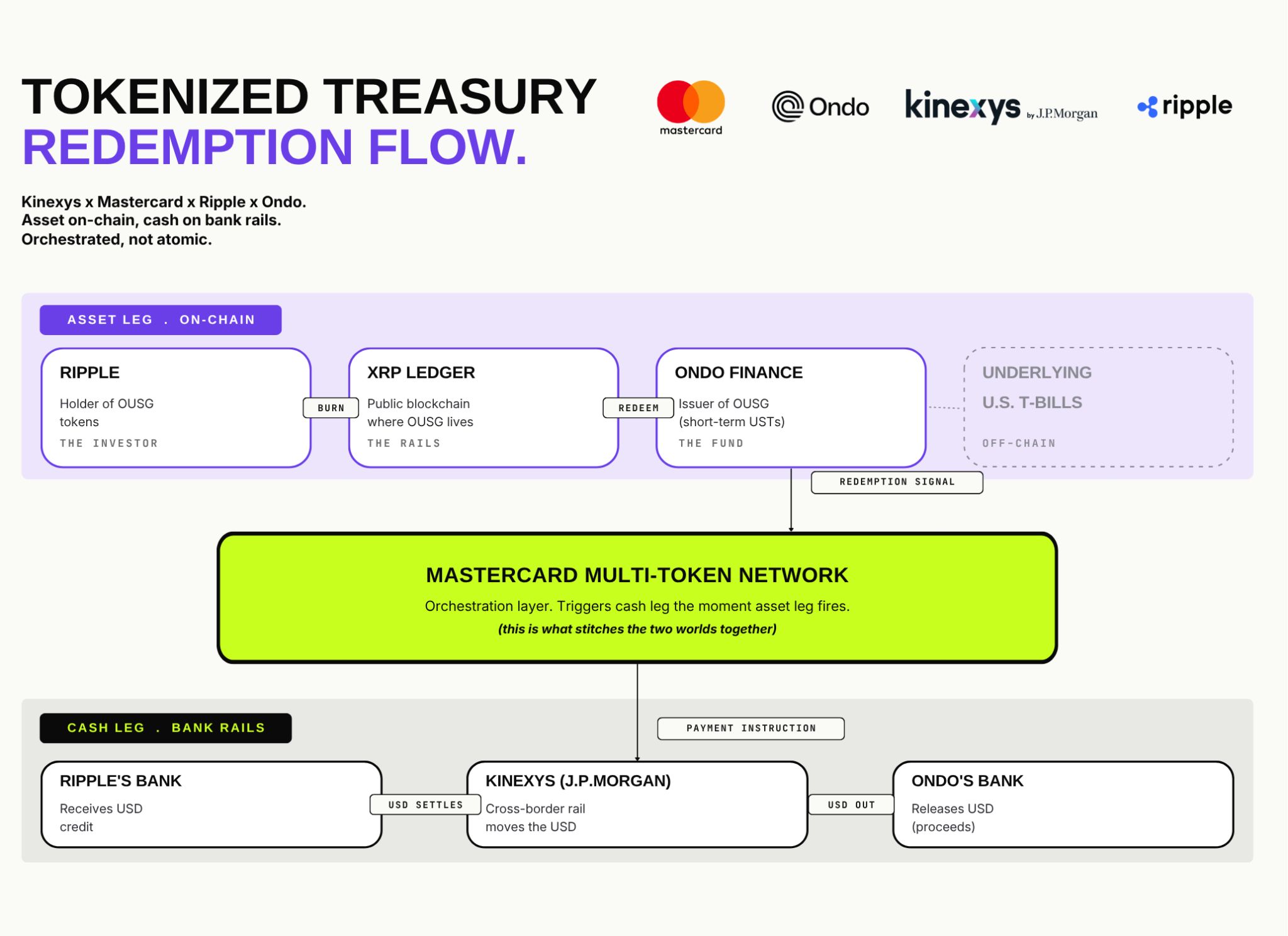

The deal is a two-world handshake. An on-chain world where the asset is born, held and extinguished, and a bank-rail world where the cash actually moves. Mastercard's Multi-Token Network is the seam. Six entities have distinct jobs, grouped into three layers.

The two lanes are connected only through Mastercard MTN. The asset and the cash do not settle atomically against each other on a shared ledger. They are choreographed. If the cash leg fails or delays, the asset leg has already extinguished the token. This is faster correspondent banking on top of public-chain redemption, not on-chain delivery versus payment.

Two parallel lanes, one orchestration layer in the middle.

Here is the wiring end to end. The asset leg lives on a public chain. The cash leg lives on bank rails. Mastercard MTN is the only component that sits in both at once.

Two analytical points the diagram makes visible:

- The lanes never meet on a shared ledger. They are stitched by MTN's payment instruction. That is choreography, not atomic delivery versus payment.

- The novel piece is the cash leg crossing two banks and one border. Tokenized Treasury redemption itself is not new; the bank-to-bank, border-to-border completion is.

Three reasons this is bigger than one redemption.

Kinexys is playing the role J.P. Morgan needs it to play if it wants to win the next decade of tokenized markets. It is not the venue. It is not the asset issuer. It is not the orchestrator. It is the bank money rail that other people's tokenized assets settle against. Ondo's OUSG is the asset. XRP Ledger is the venue. Mastercard's MTN is the orchestrator. Kinexys is the cash settlement utility in the middle of the cash leg. That is exactly the positioning J.P. Morgan needs if it wants Kinexys to become neutral infrastructure rather than a captive product line.

This is the second public-chain bridge from Kinexys in six months. JPMD went live on Base, the Coinbase Layer 2, in November 2025. Kinexys integrated with Chainlink CCIP for cross-chain DvP with Ondo OUSG late 2025. MONY, the My OnChain Net Yield Fund, launched on public Ethereum in December 2025. Now Kinexys is bridging into the XRP Ledger via Mastercard's network. The pattern is unambiguous. J.P. Morgan is no longer treating public chains as a research project. It is plumbing into all of them.

The partner stack is unusual in a way the press copy buries. Working with Ripple is notable because Ripple and J.P. Morgan have historically had no real overlap and XRP has been on the periphery of bank infrastructure conversations. Working with Mastercard's MTN puts Kinexys adjacent to the card networks' tokenization play, where Mastercard MTN and Visa's Tokenized Asset Platform have until now looked like a competing camp. This pilot collapses both boundaries in a single transaction.

Four qualifiers in the headline. Only one earns its keep.

The press headline is "first near real time, cross border, cross bank redemption of a tokenized Treasury fund." That phrase stacks four qualifiers on each other and they do not all earn their keep.

| Qualifier | Status | Verdict |

|---|---|---|

| Tokenized Treasury redemption | Shipped | Not new. OUSG, BUIDL, BENJI and USYC have all run redemption flows. |

| Near real time | Shipped | Not new in isolation. Kinexys settles intraday; MTN messages in seconds; XRP Ledger finalizes in 3 to 5s. |

| Cross border | Shipped | Routine for Kinexys. Multi-currency wholesale flows have run for years. |

| Cross bank | Shipped | The wedge. First redemption across institutions, borders and networks at this scale. |

Strip the other three qualifiers and what was demonstrated is a tokenized fund redemption where the cash leg crossed at least two banks and one border, synchronized through a payment network, in near real time. A meaningful but narrow first.

The hedge buried in the press release earns its own section.

The MarketWatch piece hedges in one sentence: "The process wasn't entirely decentralized: the dollar payment received for the tokenized Treasurys still moved through the traditional financial system." That hedge is load-bearing. Take it seriously.

- The asset and cash legs never met atomically. Full DvP would require cash on the same ledger as the asset (a stablecoin or deposit token native to XRP Ledger) or a cross-chain hashed time-locked settlement on both sides. Neither is what happened here.

- Latency-window counterparty risk is real. Between the OUSG burn and the USD arrival, Ripple held a claim on Ondo's bank, intermediated through Kinexys. Fine when both sides are sophisticated and latency is in minutes. Not equivalent to atomic settlement.

- This is a pilot, not a production rail. One redemption leg. No daily volume. The proof is operational, not commercial.

- The addressable market is concentrated. Total tokenized Treasurys outstanding sit at roughly $15B per RWA.xyz, mostly inside BUIDL, BENJI, OUSG and USYC with concentrated holders.

- The Clarity Act is the gating regulatory event. The technology side of institutional tokenization is largely solved. The legal and capital treatment side is not. Until the Senate moves, every pilot of this kind is a positioning artifact more than a production rail.

DTCC's October launch is the actual gating event.

The most important sentence in the source article is one most readers will skim past: the Depository Trust and Clearing Corporation announced this week it will go live with a new tokenization service in October 2026, with permission to tokenize Treasury bills and bonds among other real-world assets. DTCC sits at the center of the U.S. settlement perimeter. If DTCC is tokenizing Treasurys natively, then Kinexys, BNY, Goldman's Digital Asset Platform, Broadridge's Distributed Ledger Repo platform and the rest are no longer competing to be the venue. They are competing to be the cash and orchestration layers around DTCC's asset tokens.

Read in that light, this Kinexys pilot is a positioning move ahead of DTCC's go-live, not just a partnership announcement. It demonstrates that Kinexys can be the bank-money leg for a tokenized Treasury redemption that originates outside DTCC's perimeter, on a public blockchain, with a non-bank holder, in a foreign currency. That is exactly the proof point J.P. Morgan needs if it wants Kinexys to be the default cash rail for whatever DTCC, Nasdaq, and the buy side eventually issue on-chain.

It also fits the broader 2025-2026 wave. The GENIUS Act passed in July 2025, preserving deposit tokens as a separate regulatory category from stablecoins and giving JPMD legal cover to be yield-bearing. The FDIC opened a notice of proposed rulemaking on tokenized deposits in December 2025. The Basel Committee refined its capital treatment of tokenized traditional assets in January 2026. Project Agorá at the BIS and Project Guardian's tokenized bank liabilities workstream both expanded their bank participant lists through 2025. The picture is one of regulators slowly closing the gap between the legal category of bank money and the technical category of on-chain assets, and banks racing to be on the right side of that gap when it closes.

Modest as a breakthrough. Important as a positioning signal.

The pilot does not prove atomic on-chain delivery versus payment, does not move material volume, and does not bypass correspondent banking. The cross-bank qualifier is the only one in the headline that earns its keep. But the pilot confirms that J.P. Morgan is committing to the neutral cash utility thesis across public chains rather than the captive private chain thesis, and it lines up Kinexys as the bank-money rail for a world where DTCC, Nasdaq, Ondo, BlackRock and Franklin tokenize the asset side.

Watch three things over the next six months:

- The Clarity Act in the U.S. Senate. If it passes this year, this pilot becomes the template, not the exception.

- DTCC's October 2026 tokenization launch. The proof point that determines whether Kinexys is the default cash rail or just one of several.

- The next public-chain bridge from Kinexys. After Base, Chainlink CCIP, Ethereum and now XRP Ledger, the cadence itself is the signal.

Common questions about Kinexys and tokenized Treasury settlement.

What is Kinexys?

What happened in the May 2026 Kinexys-Ondo-Ripple-Mastercard pilot?

Is this on-chain delivery versus payment (DvP)?

What is Ondo OUSG?

Why was Mastercard's MTN involved?

What is DTCC's tokenization service and how does it relate?

Suggest a news item or request a private briefing.

Public briefings publish on no fixed cadence. Private briefings, written for one institution and one decision, are part of the consulting engagement formats.

Book a discovery call